Came across this quote from Michael Lewitt of Hegemony Capital Management recently:

At some point, society has to figure out that the way an investor earns his money is even more important than the amount of money he makes. This is why human beings were vested with moral sentiments, so they could distinguish the quality of human conduct from the quantity of its results.

hmm. An interesting idea, and one that garners some attention in a climate like this one. I don't think it would hold water in a bull market, say what you will about moral sentiments, but a very interesting thought to say the least...

Tuesday, September 30, 2008

Does This Work?

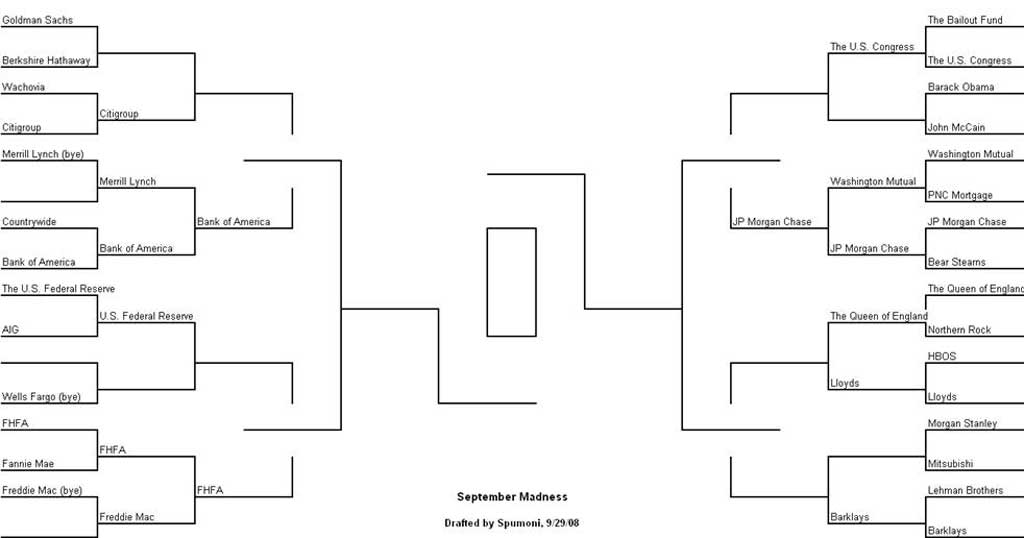

How To Get Your March Madness Fix In September

There is no better time in the sporting calendar than the first weekend of March Madness. It can be a long wait year over year, especially if your bracket gets blown out early. So what is one to do in the downtime, especially when the Giants and A's can't make the playoffs, the Olympics are over, the Raiders and 49ers are struggling at best, and you don't give a rip about hockey?

Play September Madness, of course.

How Big Is This Bailout?

Bailouts are nothing new, history has many examples. Some recent ones are explored below courtesy of ProPublica, and are put into perspective in terms of their size with a nice visual. If any of the links are broken, view them here.

With the flurry of recent government bailouts, we decided to try to put them in perspective. The circles below represent the size of U.S. government bailout, calculated in 2008 dollars. They are also in chronological order. Our chart focuses on U.S. government bailouts of U.S. corporations (and one city). We have not included instances where the U.S. government aided other nations.

Check out how the Treasury did in the end after initial government outlays.

| Industry/Corporation | Year | What Happened | Cost in 2008 U.S. Dollars | |

|---|---|---|---|---|

| ● | Penn Central Railroad | 1970 | In May 1970, Penn Central Railroad, then on the verge of bankruptcy, appealed to the Federal Reserve for aid on the grounds that it provided crucial national defense transportation services. The Nixon administration and the Federal Reserve supported providing financial assistance to Penn Central, but Congress refused to adopt the measure. Penn Central declared bankruptcy on June 21, 1970, which freed the corporation from its commercial paper obligations. To counteract the devastating ripple effects to the money market, the Federal Reserve Board told commercial banks it would provide the reserves needed to allow them to meet the credit needs of their customers. (What happened after the bailout?) | $3.2 billion |

| ● | Lockheed | 1971 | In August 1971, Congress passed the Emergency Loan Guarantee Act, which could provide funds to any major business enterprise in crisis. Lockheed was the first recipient. Its failure would have meant significant job loss in California, a loss to the GNP and an impact on national defense. (What happened after the bailout?) | $1.4 billion |

| ● | Franklin National Bank | 1974 | In the first five months of 1974 the bank lost $63.6 million. The Federal Reserve stepped in with a loan of $1.75 billion. (What happened after the bailout?) | $7.7 billion |

| ● | New York City | 1975 | During the 1970s, New York City became over-extended and entered a period of financial crisis. In 1975 President Ford signed the New York City Seasonal Financing Act, which released $2.3 billion in loans to the city. (What happened after the bailout?) | $9.4 billion |

| ● | Chrysler | 1980 | In 1979 Chrysler suffered a loss of $1.1 billion. That year the corporation requested aid from the government. In 1980 the Chrysler Loan Guarantee Act was passed, which provided $1.5 billion in loans to rescue Chrysler from insolvency. In addition, the government's aid was to be matched by U.S. and foreign banks. (What happened after the bailout?) | $3.9 billion |

| ● | Continental Illinois National Bank and Trust Company | 1984 | Then the nation's eighth largest bank, Continental Illinois had suffered significant losses after purchasing $1 billion in energy loans from the failed Penn Square Bank of Oklahoma. The FDIC and Federal Reserve devised a plan to rescue the bank that included replacing the bank's top executives. (What happened after the bailout?) | $9.5 billion |

| ● | Savings & Loan | 1989 | After the widespread failure of savings and loan institutions, President George H. W. Bush signed and Congress enacted the Financial Institutions Reform Recovery and Enforcement Act in 1989. (What happened after the bailout?) | $293.8 billion |

| ● | Airline Industry | 2001 | The terrorist attacks of September 11 crippled an already financially troubled industry. To bail out the airlines, President Bush signed into law the Air Transportation Safety and Stabilization Act, which compensated airlines for the mandatory grounding of aircraft after the attacks. The act released $5 billion in compensation and an additional $10 billion in loan guarantees or other federal credit instruments. (What happened after the bailout?) | $18.6 billion |

| ● | Bear Stearns | 2008 | JP Morgan Chase and the federal government bailed out Bear Stearns when the financial giant neared collapse. JP Morgan purchased Bear Stearns for $236 million; the Federal Reserve provided a $30 billion credit line to ensure the sale could move forward. | $30 billion |

| ● | Fannie Mae / Freddie Mac | 2008 | The near collapse of two of the nation's largest housing finance entities was yet another symptom of the subprime mortgage and housing market crisis. In an effort to prevent further turmoil within the financial market, the U.S. government seized control of Fannie Mae and Freddie Mac and guaranteed up to $100 billion for each company to ensure they would not fall into bankruptcy. | $200 billion |

| ● | American International Group (A.I.G.) | 2008 | When AIG was unable to secure a private-sector loan, the federal government intervened by seizing control of the insurance giant. | $85 billion |

| ● | Auto Industry | 2008 | In late September 2008, Congress approved a more than $630 billion spending bill, which included a measure for $25 billion in loans to the auto industry. These low-interest loans are intended to aid the industry in its push to build more fuel-efficient, environmentally-friendly vehicles. The Detroit 3 -- General Motors, Ford and Chrysler -- will be the primary beneficiaries. | $25 billion |

| ● | Troubled Asset Relief Program | 2008 | The Bush administration has proposed a rescue plan to ease the current crisis on Wall Street. If approved by Congress, the Treasury Department will be authorized to purchase up to $700 billion of distressed mortgage-backed securities and other assets and then resell the mortgages to investors. | $700 billion |

Monday, September 29, 2008

Quick Details On Bailout Plan's Unsuccessful Vote

BOTTOM LINE: House vote on TARP failed 205-228. We expect legislation to reemerge in the near future, but the extent of the modications that will be necessary is unclear. There still appears to be a good chance that Congress enacts some type of stabilization package before the election. Another vote is possible in the House later this week -- perhaps on Thursday -- but the situation is fluid.

KEY POINTS:

1. A simple majority was needed to pass the TARP plan. 140 Democrats voted in favor, and 66 Republicans supported the bill, leaving the bill 12 votes short. Internal vote counts prior to the vote expected roughly that number of Democrats to vote for the bill, but expected a greater number of Republican votes than materialized. Assuming that Democratic votes on the bill do not change, House Republicans are likely to be the key to unlocking additional support for the bill, so the focus over coming days is likely to be on what additional concessions they may request.

2. Congress will be in recess on Tuesday, and will return to legislative business on Wednesday. Another vote then is possible, but looks likely to occur at earliest on Thursday. It is not clear whether major concessions will be necessary, or whether minor changes to the bill would be enough to secure the incremental votes necessary for passage.

3. The House can bring the bill up quickly if a compromise is reached among House and Senate leaders and the White House on potential modifications. If the House is able to pass an amended plan later this week, the Senate should prove to be less challenging. However, the legislative process in the Senate takes at least two days for procedural reasons, so passage in both chambers by the end of the week could be a challenge.

Sunday, September 28, 2008

Interesting That This "Crisis" Is Happening During An Election Year

Just because of the way it shapes the discourse on the matter, the way it causes the public to value the players and the voices, the way it will shape the election, and how the election will shape the eventual path forward. I watched most of the McCain / Obama debate last week, and I have to say, when asked about their opinions on the bailout plans, I felt embarrassed that either tried to express any opinion whatsoever. Henry Paulson's request for $700bn came with a "trust me, I know what I am doing" style plea, there wasn't much to make an opinion of. Most of congress seemed perplexed by the details, so why should Obama or McCain represent to have a grasp of what it entailed, and then elaborate? Why can't they just say "I dunno, my economists will advise me on that when the details become more clear..."?

The republicans have voted down the bailout plan. The market is in a panic-style reaction. Stocks are way down, treasuries are way up, flight to safety. Even if some of them support the bailout effort, they all know that if they allow it to pass on a democrat-carried vote, McCain can soapbox all the way to the November election about how the democrats are bailing out Wall Street. You have to wonder what this would have looked like if it happend after the election...

Here are some more politically charged items floating around my desk today:

1- NY Times article dated 9 years ago tomorrow, talks about the Clinton Administration urging FannieMae to make more subprime loans. From the article:

"The action, which will begin as a pilot program involving 24 banks in 15 markets -- including the New York metropolitan region -- will encourage those banks to extend home mortgages to individuals whose credit is generally not good enough to qualify for conventional loans. Fannie Mae officials say they hope to make it a nationwide program by next spring."

2- Ron Paul preaching tough medicine in today's bailout plan vote.

3- On the fall of Lehman Brothers, Bill Bonner writes:

"... how a company that survived the Civil War, the railroad bankruptcies, the panics, WWI, the Great Depression, WWII, and the Cold War couldn't survive the biggest financial boom in Wall Street history?..."

In fairness, they survived the boom, just not the bust. But thought-provoking enough... well said.

Friday, September 26, 2008

Where Are California's Most Undervalued Real Estate Markets?

According to the Sept 10 Kiplinger Letter, which they admit may surprise some, they are:

San Diego 17.2% undervalued!

San Francisco 15.9% undervalued!

Stockton 13.8% undervalued!

Vallejo 13.4% undervalued!

Modesto 12.9% undervalued!

Santa Ana/Anaheim 12.4% undervalued!

Santa Barbara 12.3% undervalued!

Sacramento 11.1% undervalued!

Despite the fact that some of these areas are known to have some of the worst subprime mortgage problems, Global Insight (a forecaster) suggests that they have relatively healthy economies, strong job growth to support demand, and home prices have already dropped significantly.

hmmm... signs of a bottom? or overly optimistic?

Tuesday, September 23, 2008

Buy And Bail vs Note Modification

If you bought your home sometime in 2005 or 2006, you likely nailed it at the peak, depending on exactly where and exactly when you bought. And if your home has lost a significant amount of value, you have to wonder why you are still paying the bill for the mortgage, especially if the mortgage is bigger than the value of your home.

If you bought your home sometime in 2005 or 2006, you likely nailed it at the peak, depending on exactly where and exactly when you bought. And if your home has lost a significant amount of value, you have to wonder why you are still paying the bill for the mortgage, especially if the mortgage is bigger than the value of your home.

So what can you do?

+One option is to stick it out. Do nothing. Keep paying and stay put until the home value comes back... how ever long that ends up taking.

+Another is to attempt a short sale, where your lender agrees to let you sell your home for less than the balance owed on the note, and then be forgiven of any debt you cannot pay off with the proceeds from the sale.

+Less appealing is foreclosure. Let the bank take your home, walk away, etc. Bank's problem now. Your credit will be trashed, but you won't keep bleeding cash into a bad investment. Hope you can find a new home (even a place to rent) with that new 500 FICO score...

+Enter the Buy & Bail strategy. Buy a new home now, and once it closes, let the old one go into foreclosure. This sounds nice if you bought your home for $1MM, and now the one next door is selling for $600k. The problem is, your new lender wants to make sure you can afford the payments on both homes. So you try to off-set the costs of the home you will depart by bringing in a renter. If you can find one.

This might have worked, except that banks are concerned about fraud when you claim a renter who may just be a straw person, or suggest you are going to rent a home, and then walk away from the obligation to repay... aka "Bail". Your intentions clearly were not honest, and the new lender now has a brand new client with a 500 FICO score. That's not what they were signing up for.

So underwriting guidelines are responding to this practice, which has been seen before in top-heavy markets, by changing the way they value that rental income. Quite simply, if you don't have at least 30% equity in the home you will be departing, you don't have adequate 'incentive' to make good on that payment. Why would you keep paying the bill? So the new lender says: rental income is worthless in this scenario.

Here is some text from a recent FHA announcement:

This will assure that a homeowner either has sufficient income to make both mortgage payments without any rental income or has an equity position not likely to result in defaulting on the mortgage on the property being vacated. In either case, this guidance is directed to preventing the practice known as “buy and bail” where the homebuyer purchases, for example, a more affordable dwelling with the intention to cease making payments on the previous mortgage.

That will break down quite a few "buy and bail" strategies for consumers who thought they were making a crafty maneuver in this challenging market.

But is there a better alternative?

Have you considered requesting a note modification? There is a bloodbath going on out there. Banks are at the epicenter. They do not want you letting your house go into foreclosure. They can't take it, literally. Maybe you bought more house than you could afford, maybe the payments skyrocketed based on a loan feature you were not informed of, maybe you lost your source of income, had a divorce, etc... you're ready to throw in the towel.

Sensitive to the threat, and also under pressure from the government banks are working with consumers to renegotiate the terms of their loans. Results can include: forgiveness of debt, restructuring of payment, reduction of rate, extension of terms, etc. Any feature of your loan can be re-written. You can contact them yourself, but you'll have much better results with an attorney in your court. Learn more about this here.

Thursday, September 11, 2008

Down Payment Assistance Programs - Updates At Legislative Level

I am breaking a long inexplicable silence here to follow up to a recent post about rules surrounding seller-funded down payment assistance programs (DAP).

What's a DAP? (or a DPA? I'm not sure if there is an official acronym; both seem prevalent at this point). With the credit markets recoiling, the ability for homebuyers to enter the market with small down payments has been hampered. Big time. Lender's simply want the borrower to have skin in the game, so that if the value drops a little, they still have incentive to keep paying back the loan.

The DAP programs that were eliminated in the recent HR 3221 Housing Bill refer to those facilitated by a charitable organization to essentially 'launder' a down payment from the seller of the home. The down payment needs to be from the buyer's funds, not the seller's. If it came from the seller, its the same as buying the house for cheaper. Proponents of DAP argue that the borrower has equity in the house, regardless of the source. Opponents claim that the fair value of the house is really the purchase price less the seller-funded down payment, or in other words, there is no equity.

FHA was allowing these programs until they realized that default rates on borrowers with DAP assistance were 3x that of borrowers who funded their own down payment.

But without DAP in the market, fewer buyers can get into the market at entry level. And if there are no first-time buyers, who do the move-up buyers sell their homes to? They don't, and all of the sudden, nobody is buying anything, and inventories skyrocket, and prices fall... sound familiar? This is the "plankton theory of housing". We need first time buyers to keep everything moving...

There are also community organizations that provide down payment assistance, but do not receive funding from the seller of the home. There is no regulation on the table to curtail these programs, and with them, buyers can still obtain 100% financing in some circumstances.

Here is the latest on the seller-funded side of the practice:

At this point the ban on the use of seller-funded down-payment assistance with FHA-backed loans takes affect October 1st. But a compromise may be in the works. HR 6694, which would allow home builders to continue funneling down-payment assistance through nonprofit groups to home buyers using FHA loans, may pass. HR 6694 would automatically allow qualified borrowers with credit scores of 680 or above to use seller-funded down-payment assistance on FHA-backed loans. Borrowers with scores between 620-680, who relied on seller-funded gifts, might be subject to higher insurance premium fees. Borrowers with scores below 620 would be excluded from using down-payment assistance until mid-2009, when HUD would be permitted to expand the program to include them if the Secretary of Housing determined it could be done without putting a dent in FHA's insurance requiring taxpayer subsidies. Chairman Barney Frank said, "The FHA loved the ban on down-payment assistance (but) hated the ban on risk-based pricing…That seemed to me to offer an opportunity. So (HR 6694) will replace both bans with middle ground.”

Subscribe to:

Comments (Atom)

{kind=link}